Unlike bonds, equities offer no return of principal dates nor contractually prescribed income payments. Contrary to the investment sales hype bombarding us daily, dividend-paying equities are not capital ‘defensive.’ Defensive for whom, we should ask.

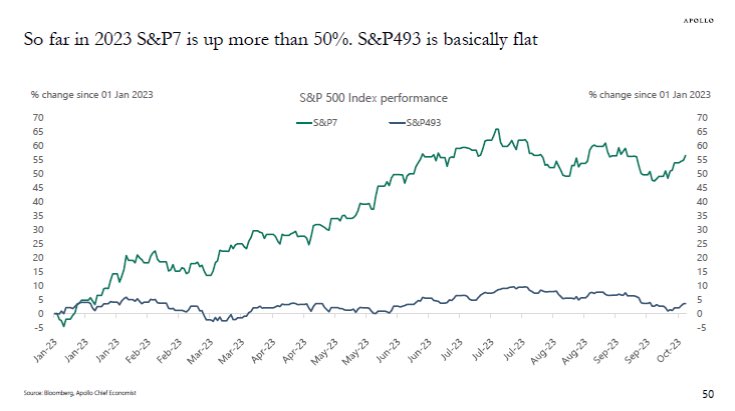

From present valuation levels, equities are priced to underperform government bonds by 6.5% annualized over the next ten years (see arrow below, courtesy of John Hussman):

“…the gap in expected returns between equities and bonds has joined the worst levels in history, matched only by extremes in mid-1929 and early-2000.” hussmanfunds.com/comment/mc2310

Komal Sri-Kumar, Sri-Kumar Global Strategies president, joins ‘Closing Bell: Overtime’ to discuss the impact of the Israel-Hamas war on inflation, what this means for fixed income returns, and more. Here is a direct video link.