Danielle was a guest with Jim Goddard on Talk Digital Network, talking about recent developments in the world economy and markets. You can listen to an audio clip of the segment here.

Follow

_________________________

Danielle was a guest with Jim Goddard on Talk Digital Network, talking about recent developments in the world economy and markets. You can listen to an audio clip of the segment here.

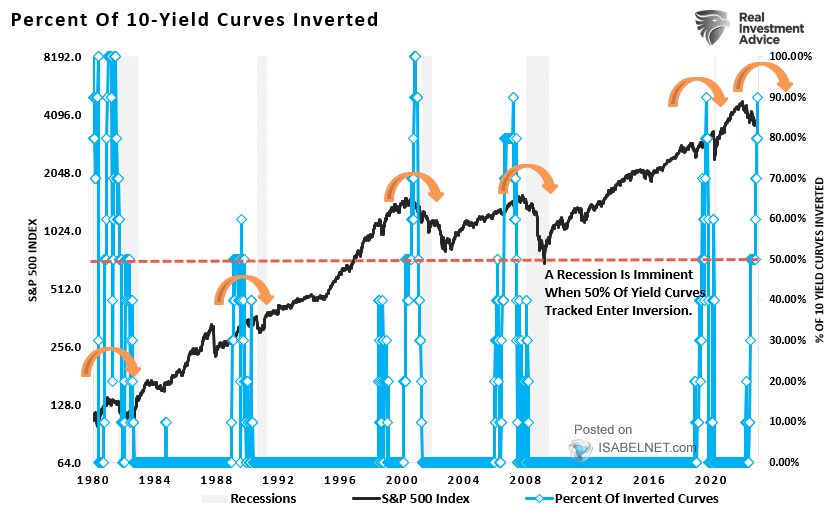

The percentage of global 2/10-year Treasury yield curves inverted at the end of 2021 (long rates lower than short) was 90% (in blue below since 1980, courtesy of Lance Roberts). Historically, recessions (grey bars) and bear markets (S&P 500 in black) have followed when the number of inverted 10-year curves reached 50% (red dotted line).

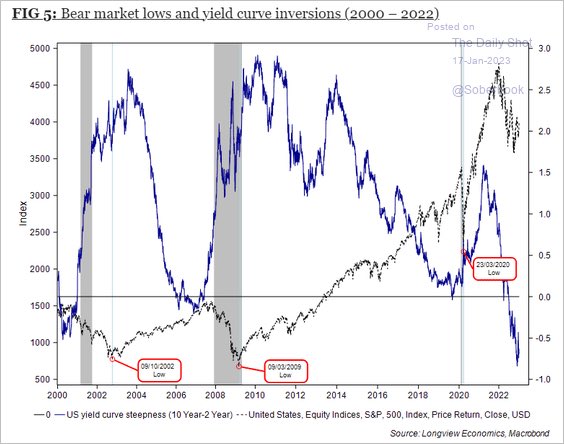

Significantly, while recessionary bear markets (S&P below in grey since 2000 from The Daily Shot) begin from inversions, stocks don’t bottom until central banks have slashed short rates enough to drop them back below long, re-steepening the curve to positive sloping once more. As shown below in blue, today, yield curves remain steeply inverted.

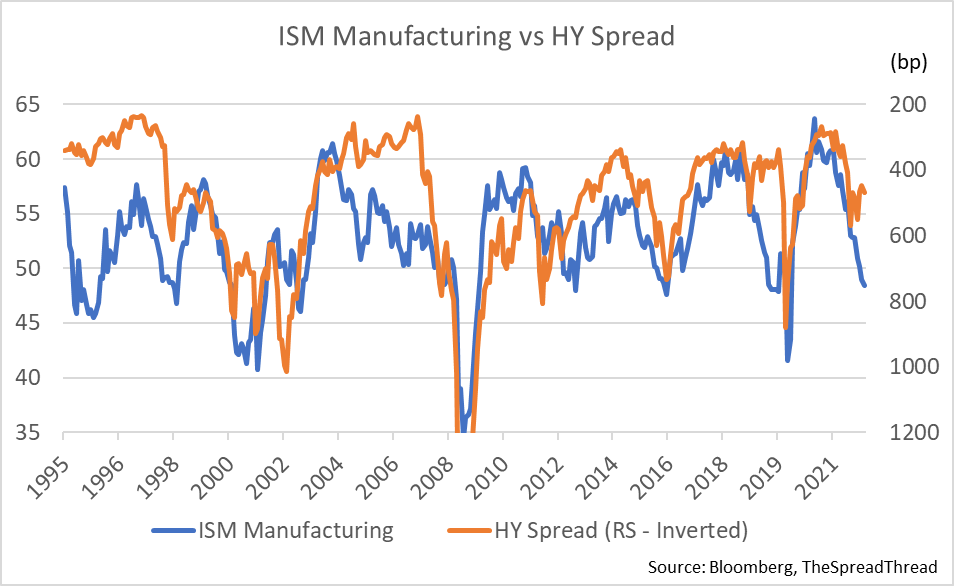

In its seventh month of inversion, yesterday’s much-watched 2/10 US Treasury yield closed at -71bps.

Meanwhile, high-yield corporate bond (HY) spreads ended yesterday at just 412 bps over similar-term treasuries. As shown below, since 1995, a contracting ISM manufacturing index (in blue) leads HY spreads wider (inverted below in orange) as defaults rise. HY bond prices typically bottom with equities once HY yield spreads have reached 800+ bps above similar-term treasuries. HY prices have much dropping yet to do.

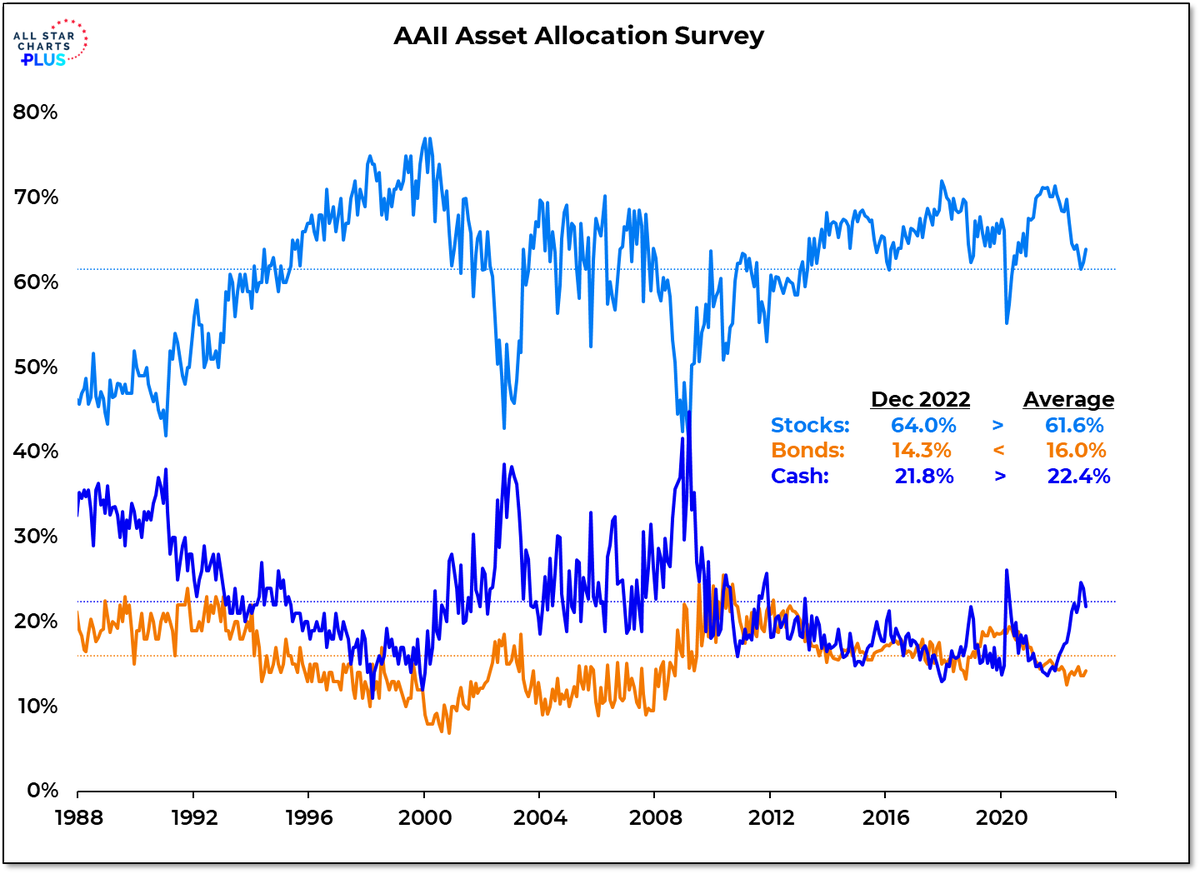

Further portfolio losses will hit hard for holders that came into 2023, 64% allocated to stocks (light blue below since 1988) with 14% in bonds (primarily corporate) and less than average cash levels. 1990, 2002 and 2009 market bottoms arrived once the allocation to stocks had fallen to 40% of portfolios.

Bottom line: no cycle bottom is yet in sight for the economy, risk assets, or the net worth of the masses. Word to the wise.

A decade of ultra-low rates punished risk-conscious savers and encouraged profligate financial decisions among the masses. Rather than use record-low interest rates to get out of debt faster, most levered up to imprudent levels. Insufficient cash and falling prices are common themes as pandemic excesses unwind. This will take some time, but for the few prepared to take advantage of the bust cycle, it’s well worth being patient. The discussion below illuminates trends unfolding in the auto market.

Car prices went bananas after COVID hit — propelled by inventory shortages from disrupted supply chains & the unprecedented stimulus sent to businesses & households. Now here in 2022, the boom may be ending. Used car prices which nearly doubled post-COVID, have fallen for much of this year — though still remain much higher than their pre-pandemic lows. Also, lax lending standards in extending auto loans during the recent boom are coming back to bite lenders — the percentage of loans that are at least 60 days delinquent hit 1.65% in the third quarter, the highest rate for 60-day delinquencies in more than a decade. Where is the auto market headed from here? Will patient buyers be rewarded with better values in 2023? Here is a direct video link.

Something not mentioned in this discussion is that the vast majority of vehicle inventories are internal combustion engines (ICE) while demand growth is focused on cheaper-to-run electric vehicles and shared transportation as a service. #ICEglut

At the same time, the unprecedented global liquidity contraction unfolding (dark blue below since 1995, courtesy of Mikael Sarwe) has historically led corporate earnings (light blue below) by 12 months. Whistling past the graveyard, equity markets are priced for earnings growth over the next year. More downside to come.