Truly other world…

Sandy Munro was blown away by Tesla’s profit margin, which is eight times more than Toyota’s. Here is a direct video link.

Truly other world…

Sandy Munro was blown away by Tesla’s profit margin, which is eight times more than Toyota’s. Here is a direct video link.

Bank economist Robert Kavcic offers useful macro housing context in the Better Dwelling segment below. One caveat worth noting, though: from a price peak in February 2022, a housing bottom by mid-2023 would be an unusually quick downcycle.

Meanwhile, the Bank of Canada’s late but great tightening from March 2022 through early 2023 will contract financial conditions through the economy until at least March 2024, even if the BOC pauses and then returns to easing later in 2023.

How much will Canadian real estate correct? Is it a bubble? BMO senior economist Robert Kavcic drops some knowledge with our team. Here is a direct video link.

In other realty news: some 17% of office space nationally is empty in Canada, see Canada’s office vacancies hit record as space floods market.

The 13.6% vacancy rate in downtown Toronto is now the highest since 2003. An additional 62% of new space under construction nationally is expected to complete in 2023.

Also, overbuilding during the credit bubble has left excess square footage and inventory amid aging populations in many countries. See, China’s Housing Market will Revive but might not thrive. There are global consequences here:

China’s long-suffering property market will finally get some relief in 2023. But it seems unlikely to ever again become the enormous structural growth driver it was for most of the past two decades—a fact that will reshape future commodity markets and how China’s growth affects the world.

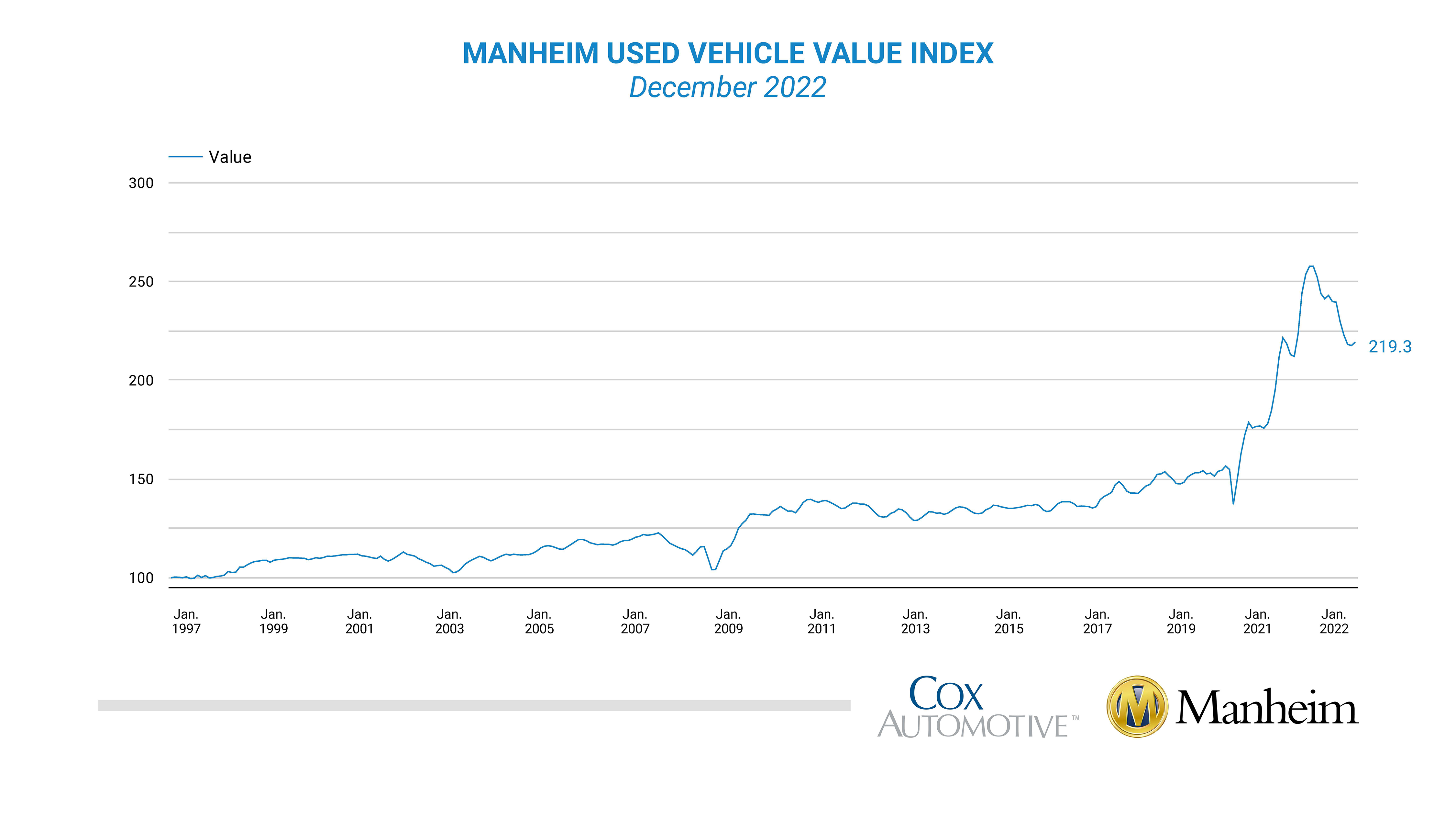

Used car prices fell nearly 15% year over year in December, and as shown below, since 1997, prices would need to fall another 30% to return to pre-COVID norms.

Monetary policy changes move through the economy in 12 to 24-month lags. This happens for a few reasons. First, many interest rates are fixed for set terms, so carrying costs do not increase or lower until a loan is renewed. Another reason for the time lag is human behaviour. People will typically keep up payments at the expense of discretionary spending and tap other credit for as long as possible. If they do fall behind, it takes time for lenders to claim any collateral, sell it, and write off deficiencies as bad debt.

Monetary policy changes move through the economy in 12 to 24-month lags. This happens for a few reasons. First, many interest rates are fixed for set terms, so carrying costs do not increase or lower until a loan is renewed. Another reason for the time lag is human behaviour. People will typically keep up payments at the expense of discretionary spending and tap other credit for as long as possible. If they do fall behind, it takes time for lenders to claim any collateral, sell it, and write off deficiencies as bad debt.

Would-be sellers are also often reluctant to admit that prices are falling. This is particularly evident in housing and big-ticket items like automobiles, where owners will keep asking above-market prices for some time in the hopes of reclaiming a past cycle peak.

Eventually, a lack of patience, financial resources, time and other constraints ultimately prompt capitulation selling and, finally, deep value for buyers. But it takes time, liquidity and discipline to take advantage of the cycle.

The segment below does an excellent job of explaining the lag between mounting inventory and falling prices in the used auto market.

Dealerships and Banks are in Trouble Dealerships Refuse to Lower car Prices. Here is a direct video link.