After the 2008 financial crisis, more than a decade of zero-interest-rate policies drove an explosion in private credit products and funds that were initially marketed to institutions and pensions under the oxymoron of safe ‘high-yield’.

Then, from March 2022 to May 2023, a record succession of central bank rate hikes took the US Fed rate from .25 to 5.25% in 14 months.

In the liquidity crunch that followed, stock prices dove, credit markets froze, and real estate entered an ongoing mean reversion. Needing cash, private funds shifted their marketing focus to retail investors as the next pool of necessary greater fools. It worked for a while.

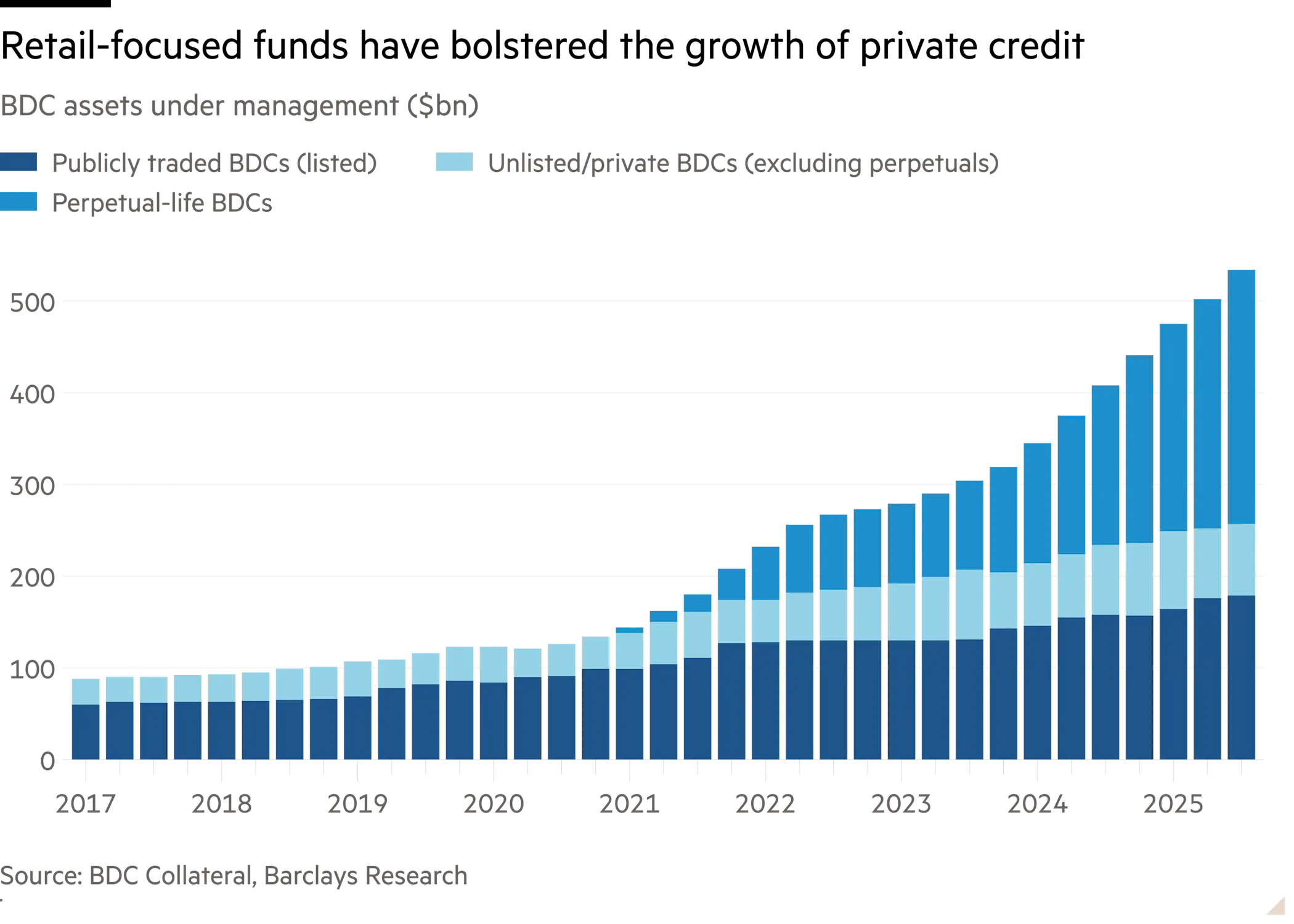

Private credit vehicles, known as semi-liquid funds, were an engine of growth for giant private investment firms, including Blackstone, Ares Management and Blue Owl, providing lucrative management fees and helping quadruple assets in BDCs [Business Development Companies] since 2021 (charted below). See, Investors ditch private credit funds on rising worries over bad loans:

See, Investors ditch private credit funds on rising worries over bad loans:

Many affluent retail investors were drawn to the space by the high dividends on offer, with annualised total returns eclipsing 8 per cent over the past decade, according to S&P Global. The recent cuts as well as asset sales at some funds “reignited credit-cycle fears” across private credit, said Paul Johnson, an analyst at KBW.

Fast forward to 2025, and investors began trying to exit private credit funds as they took losses on bad loans, and concerns intensified that AI would wreak havoc on the software companies they had financed. In response, funds have increasingly gated withdrawals and income distributions. As usual, blocking exits intensifies panic and increases the urge to get out.

Once more, investors are learning that there is no such thing as a free lunch or safe high yields. While would-be-sellers swamp willing buyers, asset prices are headed lower. The clips below discuss some of the contagion risks.

Dan Rasmussen, Verdad Capital founder, joins ‘The Exchange’ to discuss the state of the private credit market. Here is a direct video link.

“This will be a shakeout. I don’t think it is going to be short-term,” Marc Rowan, CEO and co-founder of Apollo Global Management, says during a discussion with Bloomberg News Editor-in-Chief John Micklethwait at Bloomberg Invest. Here is a direct video link.