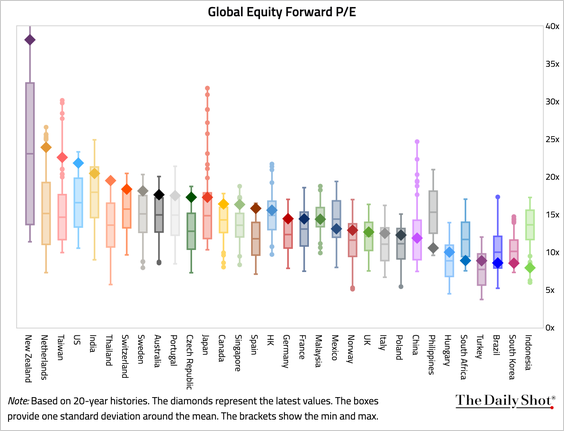

The US (in light blue below, courtesy of The Daily Shot) is at the high end (see diamond) of its 20-year forward price-to-earnings (PE) multiple, but it is not the only highly valued market today. New Zealand is the most expensive, and Canada (in yellow) is also near the high end of its historic range. Only a handful of emerging markets (on the far right of the chart) are near historic low valuations.

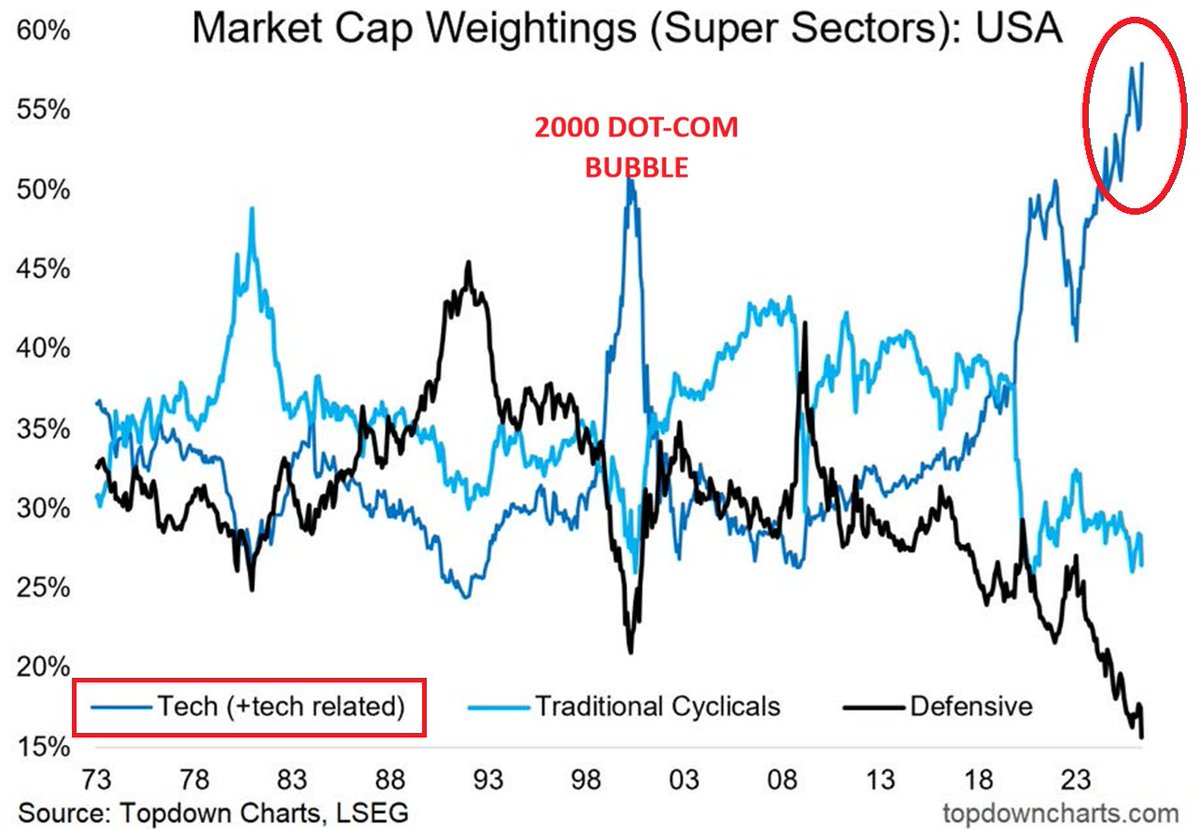

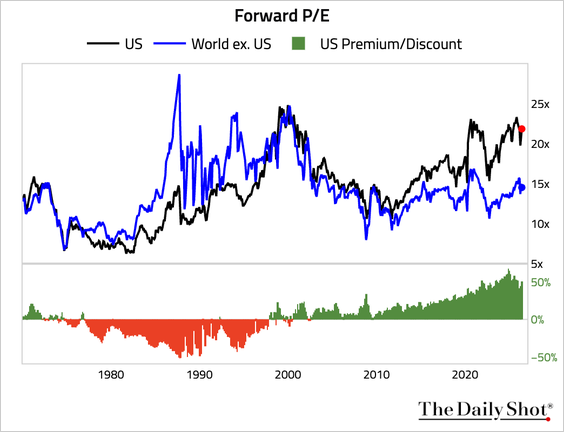

Bloated by a handful of US tech-AI cos, the premium of US stock prices over the rest of the world (below in black since 1970) is the most extreme since the 2000 tech bubble. At the end of 2025, the U.S. accounted for about 62% of the global market cap when the nine most expensive U.S. tech stocks were included, or around 41% excluding those nine mega-caps, ICAEW. The concentration is staggering. Back in 2007, the U.S. share of the global market cap peaked at 29.6% — so, it has roughly doubled since then.

At the end of 2025, the U.S. accounted for about 62% of the global market cap when the nine most expensive U.S. tech stocks were included, or around 41% excluding those nine mega-caps, ICAEW. The concentration is staggering. Back in 2007, the U.S. share of the global market cap peaked at 29.6% — so, it has roughly doubled since then.

Meaningful shelter from the popping of a US-centric stock bubble is hard to find. Global fund flows are leveraged off of one another, so when US stock prices tumble, contagion spreads as investors and speculators raise cash everywhere that they can.

Recognize it or not, we are living through one of the most extreme periods of investment risk in history. The corollary of this setup suggests that the inevitable bust will also present one of the most valuable long-term investment periods in history. The art is to be prepared and able to take advantage of it (as in 2002 and 2008) when that opportunity finally arrives. Grantham’s discussion below offers further context.

Jeremy Grantham joins Excess Returns to discuss The Making of a Permabear, mean reversion, market bubbles, AI, the Magnificent 7, and the long-term lessons investors can take from his career at GMO. We cover why he rejects the simple “permabear” label, how he thinks about valuation and bubbles, why AI may be both transformative and dangerous for investors, and why long-term thinking is so hard but so essential. Here is a direct video link.