Happy Friday!

The S&P 500 has soared over 12% since the start of April, and 7% since the start of the Iran war, thanks to a +40% rebound in chip stocks. Half the rally has been accounted for by five companies — Alphabet, Nvidia, Amazon, Broadcom, and Apple. At the same time, broader sectors like financials have posted near-flat earnings growth, and healthcare has negative growth. If we weight all 500 companies equally, the index has actually fallen slightly.

Consumer sentiment in May fell to a fresh record low of 48.2 as the US 30-year fixed mortgage rate rose above 6.5%. Homebuilder stocks are off about 20% from their 2024 highs, and consumer companies are feeling the gloom. Consumer discretionary bellwethers like Whirlpool are down 58% since last July, and McDonald’s hit a new 52-week low today, -18% since February and now back to the same level as April 2023.

“War in Iran resulted in recession-level industry decline in the U.S. as consumer confidence collapsed in late February and March.” — Marc Bitzer, CEO of Whirlpool, May 7, 2026

Consumer staples companies are generally more defensive, but the sector is down 6% since February, with companies like Heinz down 18% since last July. Kraft Heinz CEO Steve Cahillane cited struggling consumers in his earnings call this week:

“They’re literally running out of money at the end of the month. We’re seeing negative cash flows in the lower-income brackets while they’re dipping into savings.”

Gains in semiconductor stocks have pushed high-beta shares to record outperformance relative to the lower-volatility, more economically sensitive sectors of the S&P 500 (as shown below since 2014, courtesy of The Daily Number).

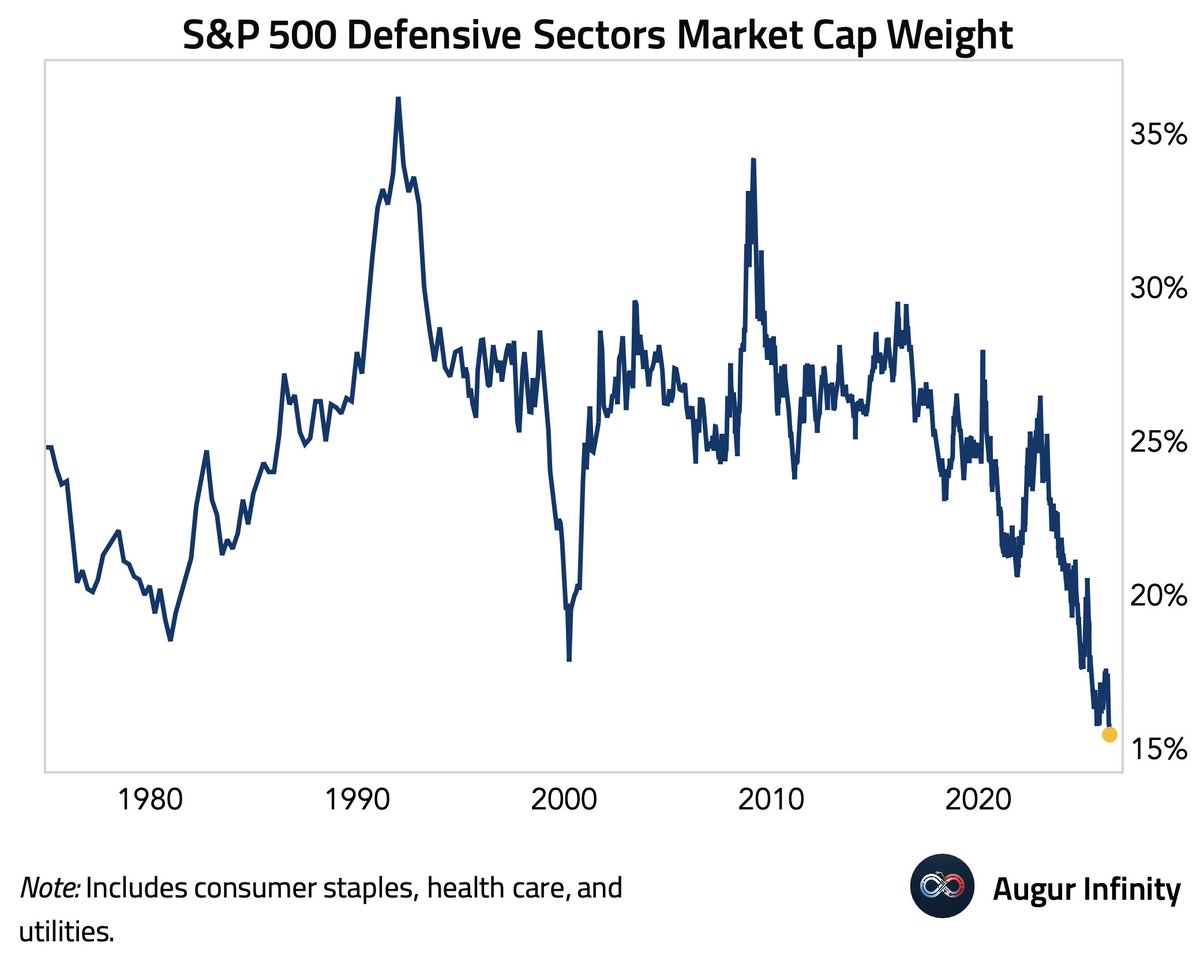

The market cap of so-called “defensive” sector stocks has fallen to a record low 15% of the S&P 500 market cap (below since 1975, courtesy of Augur Infinity). It’s not that defensive sectors are deeply discounted; it’s that the 8 most expensive companies, all in tech, have distorted the index so much that they account for a bloated 38% of the S&P 500 market cap.

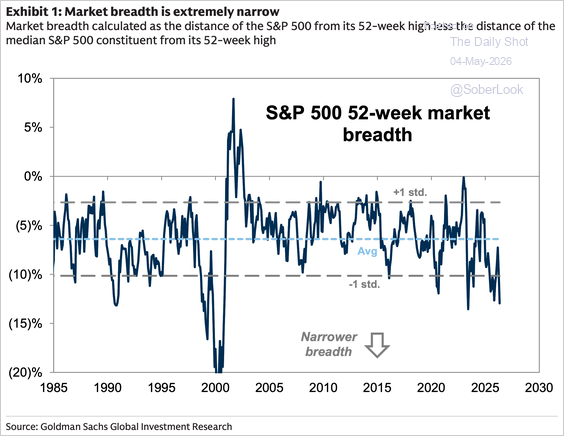

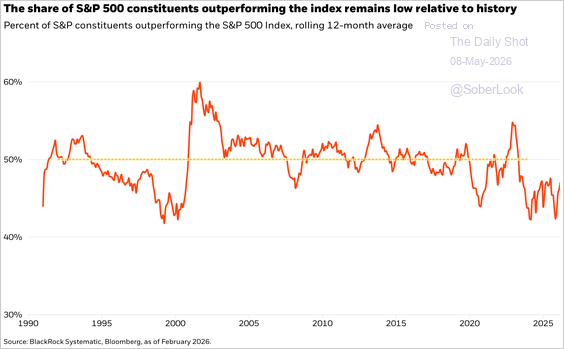

The market cap of so-called “defensive” sector stocks has fallen to a record low 15% of the S&P 500 market cap (below since 1975, courtesy of Augur Infinity). It’s not that defensive sectors are deeply discounted; it’s that the 8 most expensive companies, all in tech, have distorted the index so much that they account for a bloated 38% of the S&P 500 market cap. Another way of looking at it, market breadth is unusually weak, with the share of S&P 500 companies outperforming the index average near the lows seen in other tech-led manias in 2021 and 2000 (below since 1990, courtesy of The Daily Shot).

Another way of looking at it, market breadth is unusually weak, with the share of S&P 500 companies outperforming the index average near the lows seen in other tech-led manias in 2021 and 2000 (below since 1990, courtesy of The Daily Shot). The S&P 500’s Cyclically Adjusted Price-to-Earnings ratio (CAPE) at over 41 times is a level seen just once before at the internet-inspired bubble peak in March 2000 (shown below, since 1870).

The S&P 500’s Cyclically Adjusted Price-to-Earnings ratio (CAPE) at over 41 times is a level seen just once before at the internet-inspired bubble peak in March 2000 (shown below, since 1870). On a forward price-to-earnings basis, things are not much cheaper (as shown below, since 1960). The masses are either oblivious or don’t care because they believe that valuations no longer matter. This belief was also widely (and wrongly) held at the market peaks in 2021 and 2000.

On a forward price-to-earnings basis, things are not much cheaper (as shown below, since 1960). The masses are either oblivious or don’t care because they believe that valuations no longer matter. This belief was also widely (and wrongly) held at the market peaks in 2021 and 2000. For an excellent overview, see Greg Ip’s, AI Is Distorting Practically Everything About the Economy;

For an excellent overview, see Greg Ip’s, AI Is Distorting Practically Everything About the Economy;

Start with the broadest measure of growth, inflation-adjusted GDP. It grew a respectable 2% annualized in the first quarter. Beneath the surface, though, are two economies: AI and everything else.

Personal consumption, the biggest component of GDP, grew a relatively muted 1.6%. Investment fell in housing, business structures such as office buildings and factories, and transportation equipment like trucks and aircraft. Meanwhile, investment soared 43% in tech equipment, 23% in software and 22% in data-center buildings.

My back-of-the-envelope estimate is that the AI economy grew 31%, the non-AI economy just 0.1%.

It’s unclear how long Artificial Intelligence can replace human workers and sustain an economy dependent on growing consumer demand. AI certainly doesn’t buy financial assets and homes. Something’s gotta give. Ponzi schemes can only continue until a growing share of investors ask to sell or make withdrawals. And with each passing day, more and more people are.