The Canadian Real Estate Association (CREA) has downgraded its forecast for home sales in 2026, while the number of homes sold across the country in March fell 2.3% from a year earlier. See, CREA lowers home sales forecast for 2026 amid ‘shaky’ economic start to year.

CREA now expects a total of 474,972 residential properties to be sold in 2026, 1% more than in 2025, and down 30% from the cycle peak of 667,000 home sales in 2021.

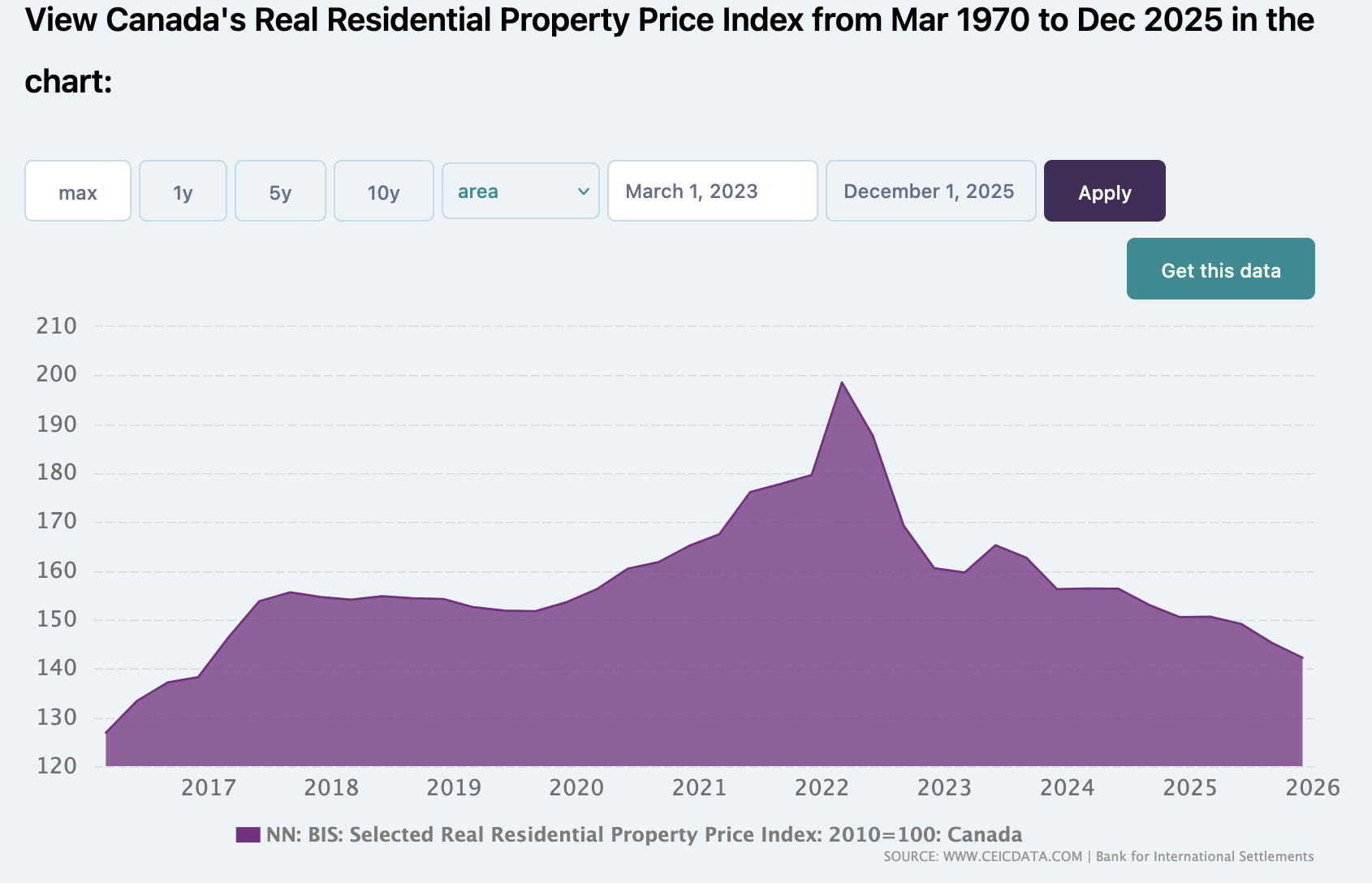

In March, the national average sale price fell 0.8% from a year earlier to $673,084, down 18% in nominal terms and about -30% in real terms from the peak of $816,720 in February 2022. Nationally, the nominal Canadian average home sale price is back to its 2021 level. On a real basis, Canadian home prices have retraced 9 years to 2017 levels (shown below, courtesy of CEIC data and the BIS).

The organization of realtors expects the national average sale price to rise 1.5% to $688,955 in 2026 — about $10,000 lower than their January forecast.

The organization of realtors expects the national average sale price to rise 1.5% to $688,955 in 2026 — about $10,000 lower than their January forecast.

On current forecasts, 2022 peak prices are not expected to be recouped in nominal terms until 2029 (WOWA).

After the 1989 bubble peak, home prices in the Greater Toronto Area (GTA) fell 28.5% in nominal terms until 1995. In real (inflation-adjusted) terms, prices did not return to their 1989 highs until 2011 — 22 years later.

China has been leading a global real estate cycle down after its massive property bubble burst in 2021. By 2023, Chinese housing starts had dropped more than 60% from pre-pandemic levels, marking one of the largest housing busts globally in decades.

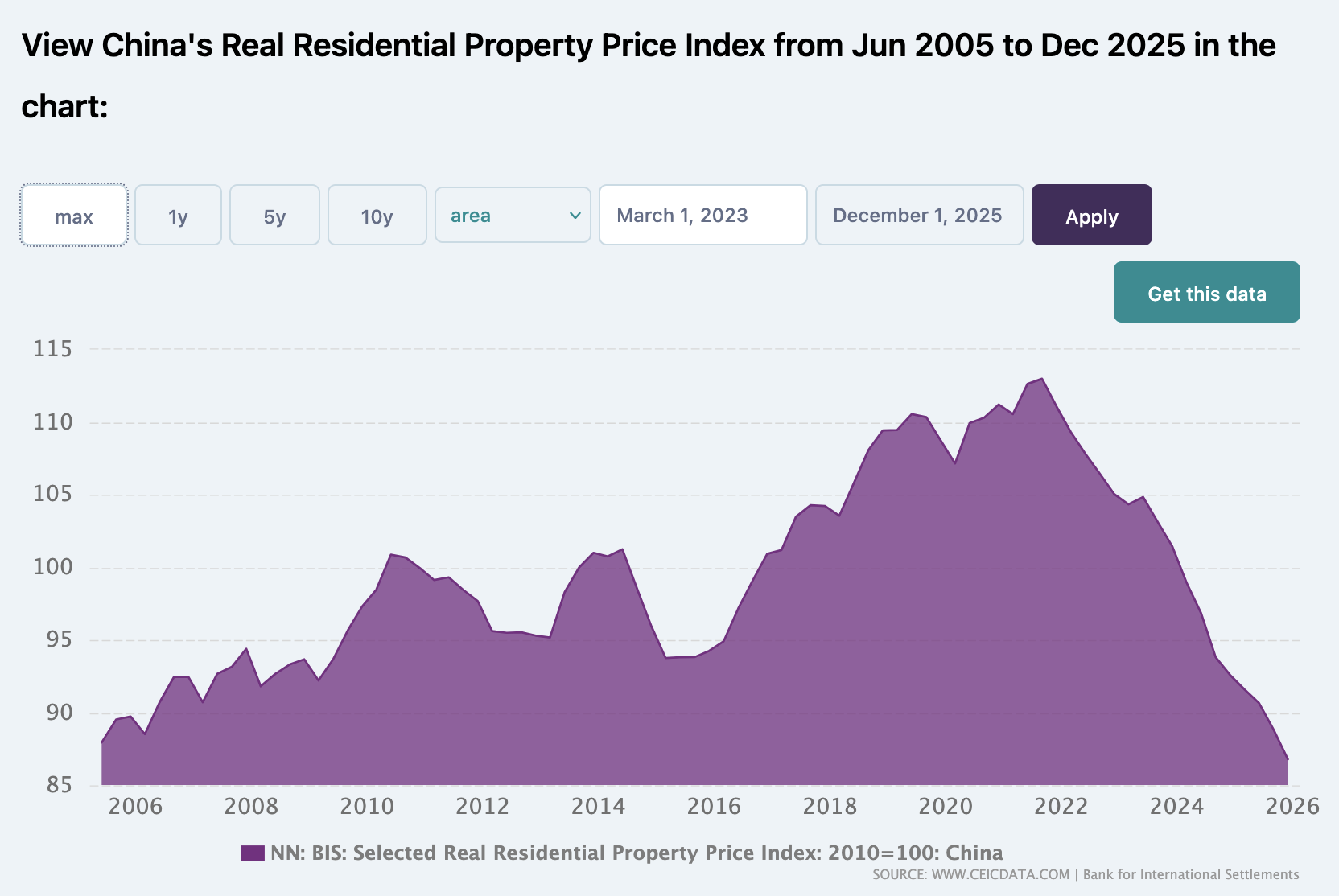

China’s real residential property price index has seen a record 17 consecutive quarters of decline. In real terms, home values are now where they were in 2006, wiping out 20 years of appreciation for the country’s urban middle class (below via CEIC and the BIS).

There are some striking similarities between fiscal and monetary policy choices made in China and Canada. The following summary should ring some bells for Canadians, see Is China’s economic resilience masking a real estate collapse:

China’s current property crisis stems from the central role of real estate in its economy, which drove rapid growth and contributed about 20% of economic activity. For a decade before the pandemic, housing prices surged relative to household incomes, partly because consumers, facing limited attractive savings options, increasingly invested in property. This fueled heavy borrowing by developers, while local governments became dependent on land sales for revenue.

In 2020, to address concerns about the overheating market, the Chinese authorities introduced the “Three Red Lines” policy aimed at curbing speculative behavior and excessive corporate debt. The policy imposed strict limits on developers’ leverage and liquidity, while banks were restricted from lending to these firms. This credit squeeze then contributed to the collapse of overleveraged developers.

…As property sales plummeted, many developers who relied on pre-sales to finance construction struggled to finish projects. In response, numerous homebuyers launched a “mortgage boycott”, refusing to make payments on unfinished apartments.

This decline was exacerbated by homebuyers’ concerns about developers’ financial health and uncertain property prices, with demand reaching a 13-year low.

In many countries where prices ballooned before the pandemic, home affordability remains untenable for the masses, suggesting prices have further to retrace.

EPB Macro is tracking similar implications for American home prices, employment and the economy, in The Housing Recession That Never Came — And The One That’s Quietly Underway. Here’s a taste:

“…with the affordability problem in the housing market still extreme, the pace of new home sales will remain sluggish, forcing companies to continue reducing construction activity or carry even more completed inventory.

In either case, the residential construction cycle still hasn’t turned higher. It’s been the same cycle since 2022, just massively drawn out by major construction backlogs and extreme profit margins in the aftermath of the pandemic.

The broader economy will be relatively unimpacted until we see the cycle play out further in residential construction, with material job losses, because it’s the early-stage job losses in sectors like construction that create the problems for the rest of the economy.”

Baby boomers are today aged 63 to 80 and will all be over 65 within 4 years. This cohort owns the largest share of real estate and stock market assets, and they are increasingly looking to downsize holdings to reduce risk, upkeep and overhead, while increasing free cash flow. They need able buyers. Prices lie somewhere between what current owners hope to sell at and what younger cohorts are able and willing to pay.