Danielle DiMartino Booth joins WTFinance to talk possibility of recession. Here is a direct video link.

Follow

_________________________

Danielle DiMartino Booth joins WTFinance to talk possibility of recession. Here is a direct video link.

All the hype about cryptocurrencies being more secure than conventional currencies and banks. How safe, secure and practical does all of this sound? See, ‘Bitcoin Family’ hides crypto codes etched onto metal cards on four continents after recent kidnappings:

The family’s new system involves splitting a single 24-word bitcoin seed phrase — the cryptographic key that unlocks access to their crypto holdings — into four sets of six words, each stored in a different geographic location. Some are kept digitally through blockchain-based encryption platforms, while others are etched by hand into fireproof steel plates using a hammer and letter punch, then hidden in physical locations across four continents.

“Even if someone finds 18 of the 24 words, they can’t do anything,” Taihuttu explained.

On top of that, he’s added a layer of personal encryption, swapping out select words to throw off would-be attackers. The method is simple, but effective.

“You only need to remember which ones you changed,” he said.

Part of the reason for ditching hardware wallets, Taihuttu said, was a growing mistrust of third-party devices. Concerns about backdoors and remote access features — including a controversial update by Ledger in 2023 — prompted the family to abandon physical hardware altogether in favor of encrypted paper and steel backups.

While the family still holds some crypto in “hot” wallets — for daily spending or to run their algorithmic trading strategy — those funds are protected by multi-signature approvals, which require multiple parties to sign off before a transaction can be executed.

The Taihuttus use Safe — formerly Gnosis Safe — for ether and other altcoins, and similarly layered setups for Bitcoin stored on centralized platforms like Bybit.

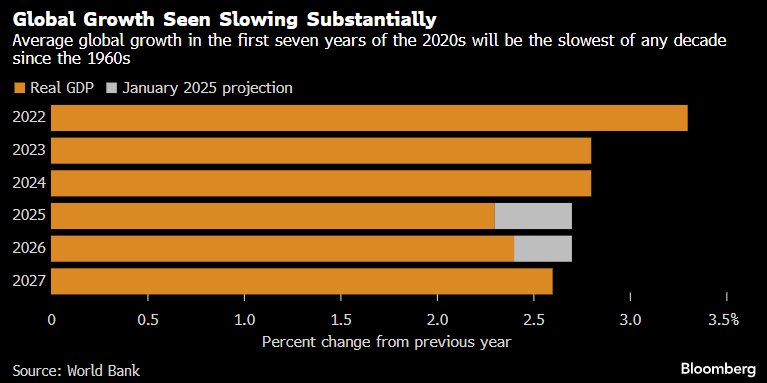

The World Bank sharply cut its global economic growth forecast.

It now projects the global economy to expand by 2.3% in 2025, down from an earlier forecast of 2.7% (below, courtesy of Bloomberg). This would mark the slowest rate of global growth, outside of a recession, since 2008. Growth is expected to recover modestly to 2.5% in 2026–2027. See, World Bank sharply cuts global growth outlook on trade turbulence:

Growth is expected to recover modestly to 2.5% in 2026–2027. See, World Bank sharply cuts global growth outlook on trade turbulence:

“Trade uncertainty, especially, has weighed on the outlook, the World Bank suggested.

“International discord — about trade, in particular — has upended many of the policy certainties that helped shrink extreme poverty and expand prosperity after the end of World War II,” Indermit Gill, senior vice president and chief economist of The World Bank Group, said in the report.

It also cut its 2025 growth forecast for the U.S. by 0.9 percentage points to 1.4%, and reduced its euro area GDP expectations by 0.3 percentage points to 0.7%.