Worried about tariff-inspired inflation, the US Federal Reserve has held its overnight target rate steady at 4.25 to 4.5% since December, and markets have walked back easing expectations to just two 25 basis point cuts by year-end.

At the same time, businesses are warning that constantly shifting trade policies are hindering their ability to plan for the future, resulting in hiring and investment freezes. See WSJ, The US economy is headed toward an uncomfortable summer:

The U.S. labour market has been in an uneasy equilibrium, where companies aren’t hiring but are reluctant to fire workers they hired three or four years ago. Like a beach ball that shoots skyward after being held underwater, joblessness can quickly jump once companies decide demand is too soft to keep those workers.

Despite the official unemployment rate still being relatively low at 4.24%, it increased in May for the 4th consecutive month, marking the highest level since October 2021. If 625,000 Americans had not given up and left the job market, the official unemployment rate would be 4.6% and already above the Fed’s peak projection of 4.4% this year.

As Rosenberg Research pointed out yesterday, Friday’s NFP US jobs estimate of +139k in May came amidst downward revisions to the prior three months, totalling -187k. In other words, benchmarked off where we were at the turn of the year, surveyed employment has contracted in 2025.

Cumulative downward revisions from January to April from the first new job estimate to last revisions, have totaled -219k or around -50k per month: “this is the same pattern of downward revisions we had in the fall of 2007, just ahead of the Great Recession, because the thing about downward revisions to the payroll data over multiple months is this: it is a leading indicator for turning points in the cycle”.

With US Federal debt at 125% of GDP, the Treasury market is currently fixated on what appears to be unbridled deficit spending plans. Federal interest expense has doubled from $508 billion in the third quarter of 2020 to $1.114 trillion in the first quarter of 2025 (shown below since 1947).

The US federal government has $10 trillion in refinancing needs over the next year alone, and as Apollo Chief Economist Torsten Slok points out, Rapidly Growing Treasury Supply Crowds Out Other Types of Credit Growth:

Over the past 12 months, roughly half of all fixed income product coming to the market has been Treasuries.

This is not healthy. Half of credit issued in the economy should not be going to the government.

The consequence is that investors need to allocate more and more dollars to finance the government rather than financing growth in the economy through loans to firms and consumers.

The bottom line is that if the level of government debt were significantly lower, more dollars would be available for consumers to buy new cars and new houses, and for companies to build new factories.

The US 10-year Treasury yield, at 4.5%, is back at the same level as early February 2025, May 2024, the fall of 2023, and July 2007, before that; US mortgage interest rates have risen along for the ride.

Not surprisingly, US consumer debt delinquencies have also been rising, raising concerns that deteriorating financial conditions will lead to a more pronounced slowdown in consumer spending.

For the housing market, the spring sales season has been a bust. The US market has nearly 500,000 more sellers than buyers, according to the real estate brokerage Redfin. That is the largest gap since its tally began in 2013 (chart below).

“The market has been at rock bottom for the last 2½ years and there was some hope that we’d get a little bit of a turnaround this year. And it’s just actually been worse than expected,” said Redfin economist Chen Zhao.

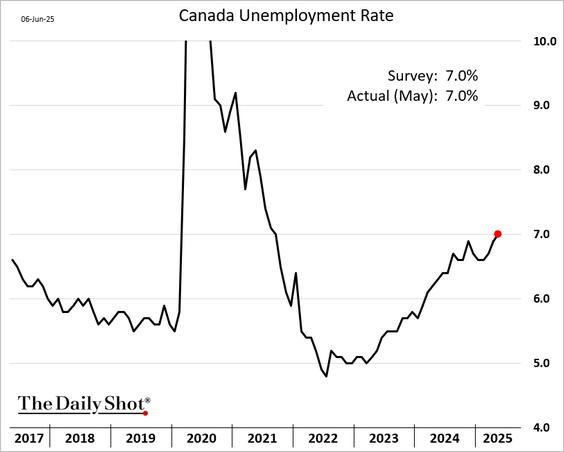

For its part, the stock market is still swinging for the fences, with Canada’s TSX near all-time highs and the S&P 5oo having recovered 20% from its April lows, even as earnings estimates have shrank for this year and next.

Wall Street has convinced itself and all who will listen that growth trends in the real economy are irrelevant to asset prices. But if valuations and economies don’t matter, why employ legions of economists, financial analysts, and investment ‘advisers’? The business model, of course, is to urge buyers at all costs and beg for government bailouts when inevitable implosions happen. Individuals are recurring collateral damage; it’s wise to be wary.